Today’s Evolving Healthcare: Specialized Assets Lead to Specialized Buyers

The healthcare sector is by no means immune to changing economic conditions, but among commercial real estate investors, medical facilities continue to be among the most popular and desirable investments. An aging U.S. population has driven demand for all types of healthcare properties – from more traditional medical office buildings, physicians’ offices and urgent care facilities, to highly specialized properties including behavioral health, post-acute care facilities and micro-hospitals. But as healthcare facilities become more specialized, we’ve seen buyers become more specialized as well.

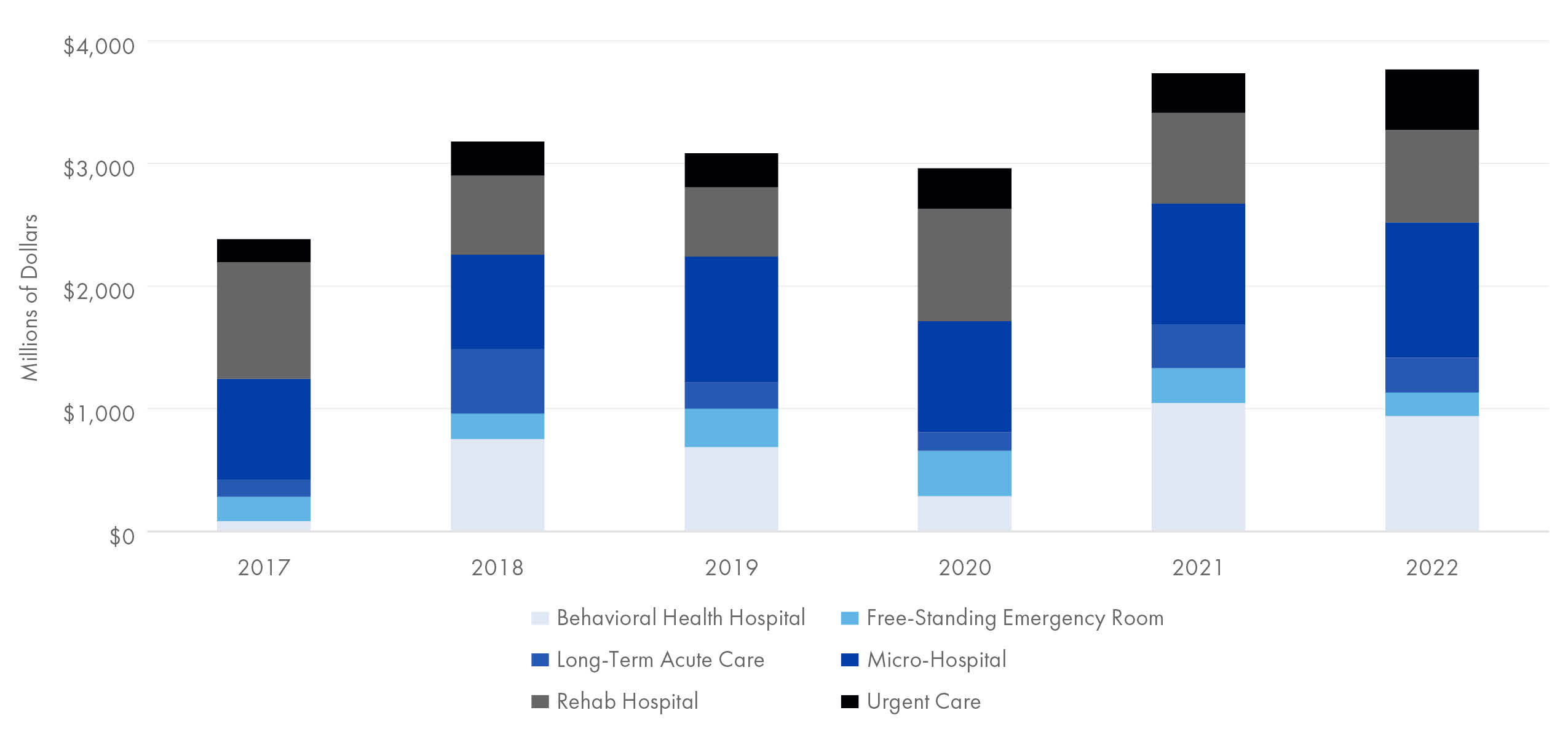

Healthcare Specialty Assets:

Investment Sales Volume

Some healthcare and medical investors see value in acquiring assets with high acuity uses and expensive finishes and build-outs. High revenue potential and replacement costs for these properties provide investors with certainty of continued use by the tenant. Other investors have become focused on properties leased to health systems and see an opportunity to foster relationships with their tenants for long-term success. Still other investor groups recognize that high construction costs have created opportunities to acquire value-add facilities, including second generation medical office buildings that are ripe for renovation or redevelopment. Regardless of an investor’s chosen lane of specialization, ever increasing demand from consumers will continue to drive the need for new healthcare facilities, creating more and more opportunities for investors to enter the sector or add to their existing portfolios.

Healthcare development is occurring throughout the U.S., as consumer demand can be found across all regions and in markets of all sizes. Unsurprisingly, the state of Florida currently leads the nation in new healthcare development. With more than 21 percent of the population over age 65, demand from retirees and aging Americans are keeping developers busy.

As these new developments come online, they’re capturing the attention of a variety of buyer groups. While REITs and institutional investors have historically been quite active in the sector, changing market dynamics have caused these buyers to become less competitive over time. The desire to acquire healthcare assets remains strong, but with more buyers now active in the sector, the available supply of properties is not enough to meet investor demand. Private equity funds, family trusts and individual investors have come to appreciate the stability and increasing demand forecasted for the sector, and REITs and institutions are simply being outbid by buyers with access to low-cost capital and a strong appetite for the product. As a result of this demand, we have seen the single-tenant healthcare sector grow in annual transaction volume, demonstrating a nearly 150 percent increase in the last ten years.

Looking ahead, however, the gap between buyer and seller expectations will cause transaction volume to decline, and activity is expected to be suppressed for at least the next 12 months. The ability to sell at unprecedented pricing is likely a thing of the past and is no longer a primary motivation for owners. Instead, in the next 18 to 36 months, conditions motivating a sale should center around debt maturity and the need to refinance. In today’s environment, sellers will need to price their assets for today’s buyers or risk chasing the market, while buyers shouldn’t ignore good fundamentals. As buyers and sellers see-saw their way closer to alignment on pricing in the coming quarters, the market can expect to see activity resume, although the lack of supply could be problematic for some time given anticipated demand.

![]()

Insights

Research to help you make knowledgeable investment decisions