Student housing investment: Key considerations for commercial real estate investors

Student housing is often grouped with multifamily. While the two share similarities, the underlying income dynamics and risk profile differ in important ways.

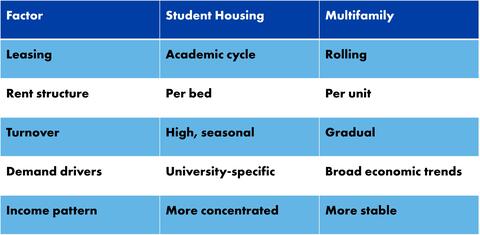

Both asset types generate rental income, but how that income is structured and how it performs over time can vary. Student housing, in particular, introduces a more defined leasing cycle and a closer tie to localized demand drivers.

For investors, the appeal is straightforward. Student housing can offer higher yields and more frequent rent resets. At the same time, those returns come with tradeoffs. Leasing timelines are more concentrated, income can be less flexible, and performance is closely tied to the strength of a specific university.

For investors, the decision centers on whether the return justifies the added risk and operational complexity.

What is student housing investment?

Student housing investment refers to acquiring or developing residential properties that serve college and university students, typically located near campus and often operated with leasing structures tailored to the academic calendar.

These properties may be purpose-built student housing designed specifically for student tenants or conventional multifamily assets that attract student renters due to proximity.

Where do the returns come from?

Student housing can generate stronger yields than traditional multifamily, but those returns are tied to specific structural factors.

Per-bed pricing

Many student housing properties lease by the bedroom rather than the unit. This structure can increase total rent per apartment, particularly in larger floorplans.

Coordinated leasing cycle

Leases are typically aligned with the academic calendar, with a large portion of units turning over at the same time each year. This creates a more concentrated leasing period compared to traditional multifamily, where leases roll throughout the year.

In strong markets, this allows rents to be reset across a significant portion of the property at once, accelerating income growth relative to assets with staggered lease expirations. In softer conditions, it can also concentrate leasing risk into a single cycle.

Localized demand drivers

Asset performance tends to be strongest in markets anchored by universities with stable or growing enrollment. In these markets, limited on-campus housing and consistent student demand can support occupancy and rent levels.

Operational intensity

Higher turnover and more active leasing cycles require increased hands-on management. For experienced operators, this added complexity can contribute to higher returns.

Where student housing investments can face challenges

The same factors that support higher returns can also introduce greater variability.

Leasing cycle exposure

Student housing operates on a defined leasing timeline. If pre-leasing activity falls short ahead of the academic year, there may be limited opportunity to recover occupancy before the term begins.

Concentrated demand

Demand is closely tied to the university. Changes in enrollment, school positioning or housing policies can influence occupancy levels. This creates a more concentrated demand profile compared to traditional multifamily.

Supply sensitivity

New development near campus can quickly increase competition. In some markets, additional supply can impact rent growth and occupancy more quickly than in broader multifamily markets.

Operational demands

Marketing, leasing and turnover are all tied to a compressed timeline. Properties require consistent coordination to maintain performance, particularly during lease-up periods.

How the student housing market is evolving

Student housing has attracted increasing attention from institutional and private capital over the past decade. As the sector has matured, more purpose-built assets have been developed in top university markets, raising both the quality of inventory and the level of competition.

At the same time, capital has become more selective. Investment activity tends to concentrate around larger universities with consistent enrollment and limited on-campus housing capacity, where performance is more predictable.

This has created a more competitive environment for both acquisitions and financing. Deals are increasingly evaluated against other asset classes, placing greater emphasis on market fundamentals, asset quality and execution strategy.

As a result, market selection plays a central role in both performance and liquidity.

Who this asset class tends to align with

Student housing can be a strong fit for certain investment strategies, but not all.

Active operators

Successful ownership typically involves a hands-on approach to leasing, marketing and asset management. Planning ahead of the academic cycle is critical.

Investors focused on local fundamentals

Outcomes are driven more by individual universities than national trends. Strong performance is often tied to:

- Large, well-established institutions

- Stable or growing enrollment

- Markets where off-campus housing remains necessary

Investors who underwrite at the campus level tend to have a clearer view of risk.

Capital targeting yield with variability

Income patterns in student housing can be less consistent year to year. Investors comfortable with that variability and focused on yield may find the asset class attractive.

Partnership-driven strategies

Many investors work with experienced student housing operators. Operational experience can play a significant role in lease-up and long-term performance.

How student housing is financed and evaluated

Financing plays a key role in how student housing deals are structured and how risk is assessed.

Agency lending remains a primary source of capital

For stabilized assets, government-sponsored enterprises such as Fannie Mae and Freddie Mac are active lenders in the space. These programs can offer competitive terms, particularly for properties with strong occupancy history and proximity to established universities.

Underwriting reflects both performance and consistency

Lenders evaluate:

- Historical occupancy and rent collections

- Pre-leasing velocity ahead of the academic year

- Year-over-year income stability

Because income is tied to leasing cycles, consistent performance often carries as much weight as peak results.

Market strength influences proceeds and structure

Assets near large, well-capitalized universities typically receive more favorable financing. Properties in less established markets may be underwritten more conservatively, which can affect leverage, pricing and structure.

Lease structure and turnover are factored into risk

Annual turnover and per-bed leasing models introduce variability that lenders incorporate into underwriting assumptions. This can influence debt sizing, reserves and overall deal structure, particularly during lease-up periods.

Execution and sponsorship matter

Borrowers with experience in student housing, or those aligned with established operators, are generally better positioned in the financing process. Lenders place significant weight on the team’s ability to manage leasing cycles and maintain occupancy.

How liquidity and exit factor in

Liquidity in student housing tends to follow market quality.

Assets located near large, well-established universities typically benefit from a deeper buyer pool, including institutional investors focused on stabilized, purpose-built properties.

In secondary or less established markets, buyer demand can be more limited. This can affect both pricing and timing at exit, particularly during periods of market volatility.

As a result, exit strategy is often closely tied to market selection at acquisition.

Student housing vs. multifamily: key differences

Understanding these differences is critical when comparing opportunities across asset types.

Is student housing a good investment?

Student housing can be an attractive option for investors seeking yield and portfolio diversification, particularly in markets anchored by strong universities.

At the same time, it requires a more active approach to asset management and a willingness to navigate variability in leasing and income.

For investors with the right operating strategy and market selection, the asset class can perform well. For those seeking more predictable cash flow with less operational involvement, traditional multifamily may be a better fit.

What to evaluate before investing

Before entering the student housing market, investors typically evaluate the following factors:

- University fundamentals: enrollment trends, funding and long-term outlook

- Supply pipeline: new development and competitive positioning

- Pre-leasing trends: early indicators of demand strength

- Asset quality and location: proximity to campus and amenity offering

- Operating partner experience: track record in student housing

These variables often have a greater impact on performance than broader market conditions.

The bottom line

Student housing is a distinct asset class with its own operating model, demand drivers and capital considerations.

It can offer strong returns in the right markets, but those returns are closely tied to execution, timing and university-specific dynamics. In a more selective capital environment, alignment between market fundamentals, financing strategy and execution plays a central role in how these investments perform.

Insights

Research to help you make knowledgeable investment decisions