Cannabis retail's next chapter: What net lease investors may be missing

For many net lease investors, cannabis retail remains a specialized asset class associated with higher risk, limited financing options and regulatory uncertainty. While those concerns have shaped the sector for years, they don't tell the whole story.

As the industry has matured, investors have gained more operating history and a better understanding of how cannabis businesses perform over time. In many cases, the questions investors ask when evaluating a cannabis retailer are not all that different from those used to evaluate franchise-owned restaurant operators or other net lease tenants. Operator strength, financial performance and long-term lease durability remain central to the investment decision.

Cannabis retail still faces challenges tied to taxation, regulation and access to capital. While cannabis real estate financing remains more complex than financing for traditional retail properties, several assumptions that have long influenced investor perceptions are becoming less clear-cut.

As investors evaluate opportunities across the net lease landscape, the question is no longer simply whether cannabis retail carries risk. It is whether perceptions of the sector have kept pace with how the market is evolving.

Cannabis real estate: Myth vs. reality

Cannabis retail has long been viewed differently than traditional net lease sectors. While some concerns remain valid, others are rooted in assumptions that don't always reflect today's market realities.

Myth: Cannabis operators are highly profitable

Many investors assume cannabis retailers generate outsized profits due to strong consumer demand. In reality, operators face significant pressure from taxation, regulatory compliance costs and competition. Performance can vary widely depending on state regulations, licensing structures and market saturation.

Reality: Revenue growth does not always translate into strong balance sheets.

Myth: Financing isn't available

Cannabis-related real estate remains more difficult to finance than traditional net lease assets, and cannabis real estate loans are often sourced through a smaller pool of lenders. However, financing is available in certain markets.

Reality: Capital is more limited, not absent.

Myth: Cannabis retail remains a fringe property type

Historically, many cannabis retailers operated in industrial corridors or secondary retail locations. Today, that picture is changing. As operators mature and consumer acceptance grows, cannabis retailers are increasingly appearing along primary retail corridors and as outlots to shopping centers.

Reality: Cannabis retail is becoming more integrated into traditional retail environments.

Myth: All cannabis operators carry the same level of risk

Just as investors differentiate between a five-unit franchisee and a 100-unit franchisee, cannabis operators vary significantly in scale, experience and financial strength.

Reality: Operator quality often matters more than industry labels.

What investors look for in a cannabis operator

Not all cannabis operators are viewed equally by investors. Larger operators with established operating histories and proven execution often attract greater investor confidence because they provide a clearer picture of financial performance and long-term stability.

Investors frequently focus on factors such as operator scale, market share, management experience and the ability to successfully navigate changing regulatory and competitive environments. As the industry matures, these business fundamentals are becoming increasingly important in underwriting decisions.

Key Takeaway: Investors are increasingly evaluating cannabis retail through the same lens used for other net lease assets: operator strength, financial performance, geographic location and lease durability.

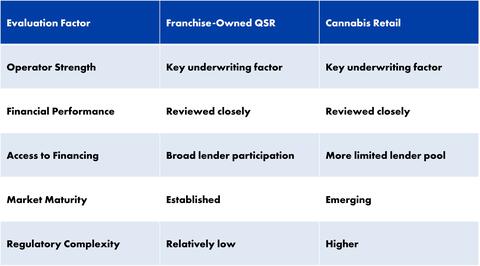

How investors evaluate cannabis real estate alongside QSR properties

Despite their differences, cannabis retailers and franchise-owned quick-service restaurants (QSRs) are often evaluated through a similar investment lens. In both sectors, investors focus on operator strength, financial performance and the tenant's ability to meet long-term lease obligations.

While cannabis retail faces unique regulatory and financing challenges, the fundamentals of underwriting remain familiar. Investors still focus on operator strength, financial performance and long-term lease durability when assessing risk.

The biggest differences between the sectors often emerge after the initial underwriting review. Financing availability, tax treatment and regulatory considerations can influence both investor demand and pricing, which helps explain why cannabis properties have historically traded at higher cap rates than many traditional net lease assets.

Not all cannabis markets are the same

Market structure can have a significant impact on investor demand and pricing.

States with limited cannabis licenses often attract stronger investor interest because barriers to entry can help support operator performance. By contrast, states with unlimited licensing may experience greater competition, making investors more selective and often requiring higher returns to compensate for perceived risk.

In limited-license states, regulators cap the number of operators that can enter the market, which can reduce competition and support stronger operator performance.

This dynamic helps explain why cannabis cap rates can vary significantly from one market to another. In some unlimited-license states, investors may seek cap rates above 10%, while limited-license markets often attract stronger demand and more aggressive pricing.

Markets drawing investor interest

While investor demand varies by market, Florida and Arizona continue to attract significant attention.

Both states benefit from population growth, favorable demographic trends and limited-license structures that can support operator performance. Florida's lack of a state income tax has also helped make the market attractive to both businesses and investors.

As a result, these markets have generally attracted stronger investor demand and lower cap rates than many states with more competitive licensing environments.

How federal changes could affect cannabis real estate financing

One of the most closely watched developments in the cannabis industry has been the federal government's movement toward reclassifying cannabis under the Controlled Substances Act. While the legal and regulatory landscape continues to evolve, the shift has prompted renewed discussion about what comes next for operators, lenders and investors.

For cannabis businesses, one of the biggest potential benefits is improved financial flexibility. Historically, federal tax treatment has limited many operators' ability to deduct ordinary business expenses, creating pressure on profitability and cash flow. Changes to that framework could strengthen balance sheets and improve operating performance across portions of the industry.

The implications extend beyond the operators themselves. Stronger financials may encourage additional lender participation, particularly from institutions that have remained cautious about entering the sector. Increased access to capital could improve financing options for both operators and investors while supporting broader market liquidity.

While the long-term impact remains uncertain, many investors are watching for signs that regulatory changes could help narrow some of the gaps that have historically separated cannabis retail from more established net lease sectors. As the market matures, investor attention may increasingly shift from regulatory concerns to the same fundamentals that drive investment decisions across the broader net lease landscape.

What cannabis real estate investors should watch over the next 12–24 months

As cannabis retail continues to evolve, investors will likely be watching several factors that could influence both risk and investment performance.

Operator quality and financial performance

As more operating history becomes available, investors may place greater emphasis on tenant-level fundamentals rather than broad assumptions about the cannabis industry. Operator experience, balance sheet strength and store-level performance will remain key considerations.

Lender participation

Access to financing has historically been more limited in the cannabis sector than in traditional net lease categories. Additional lender activity could expand financing options and improve liquidity for both operators and investors.

Regulatory and tax developments

Federal and state policy changes will continue to shape the industry's outlook. Investors should pay close attention to developments that could affect operator profitability, capital access and long-term business stability.

Competition and market saturation

Performance can vary significantly by market. Licensing structures, new store openings and local competitive dynamics may have a meaningful impact on operator success and, ultimately, property values.

Investor demand by market

Investor demand is unlikely to be evenly distributed across the country. Markets with limited-license structures, favorable demographics and population growth may continue to attract outsized investor interest compared with more saturated markets.

Continued evolution of retail locations

Investor perceptions of cannabis retail have changed significantly over the past several years. As operators continue to secure locations along primary retail corridors and within established shopping environments, investor comfort with the sector may continue to grow.

Cannabis retail is unlikely to lose its unique characteristics anytime soon. However, the industry is no longer being viewed solely through the lens of regulatory risk and limited financing. As operators mature, capital markets evolve and investor familiarity grows, cannabis retail is increasingly being evaluated on the same fundamentals that drive investment decisions across the broader net lease market.

For investors willing to look beyond outdated assumptions, the next chapter of cannabis retail may offer a very different story than the industry's early years.

Frequently asked questions about cannabis real estate financing

Is cannabis real estate financing available?

Yes. While financing options remain more limited than traditional commercial real estate sectors, community banks, credit unions and specialized lenders have become active participants in certain markets.

Why are cannabis real estate loans more difficult to obtain?

Federal regulations, lender risk tolerance and varying state laws can limit financing options. As a result, cannabis real estate loans often involve a smaller pool of lenders than traditional retail properties.

Which states attract the most cannabis real estate investment?

Investor demand varies by market, but states such as Florida and Arizona continue to attract interest due to population growth, favorable demographics and limited-license structures.

What do investors look for in a cannabis operator?

Investors typically evaluate operator experience, financial performance, market position and the ability to navigate regulatory and competitive challenges.

Looking for more insight?

Northmarq's National Net Lease & Sale Leaseback Group and National Restaurant Group help investors evaluate opportunities across emerging and established net lease sectors, including cannabis retail.

Connect with our specialists to discuss cannabis real estate financing, market trends and investment opportunities, or search our available cannabis properties today.

Insights

Research to help you make knowledgeable investment decisions