July Economic Commentary: Mid-2024 Becomes New Expected Timeline for Declining Fed Funds Rates

There were no real surprises in the economic data reported in June. Reports for some key metrics came in a bit stronger than expected, but the overall trend of a slowing economy persists. Even the labor market has started to soften, although wage growth remains elevated. Inflation pressures are easing, but the Fed is still poised to tighten monetary policy further.

Consumer Spending & Inflation

The June CPI report released on July 12 showed inflation increasing by 0.2 percent during the month, dropping the headline year-over-year number to 3.0 percent – a 27-month low. Core CPI, which strips out food and energy, also rose 0.2 percent in June, dropping the year-over-year number to 4.8 percent, which reflects a 20-month low. Even Chair Powell’s favorite inflation measure – U.S. service prices, which exclude housing and energy – increased at only 4.0 percent year-over-year, making it the slowest pace reported since the end of 2021. The big improvement in the headline CPI was due primarily to the impact of high energy prices last May dropping out of the year-over-year calculation. Assuming monthly readings of 0.2 percent for the remainder of the year, the year-over-year headline CPI should end the year around 2.7 percent.

Monthly data show that consumer spending has been basically stagnant since January. Spending in nominal terms in May was up 0.1 percent and flat in real terms. While nominal retail sales are up 1.6 percent year-over-year through May, real retail sales (adjusted for inflation) are down 2.4 percent from the previous year. Year-over-year real retail sales have been flat or negative in six out of the last seven months.

The easing in inflation pressures, coupled with continued strength in wage growth, has resulted in real disposable income growth improving to 4.0 percent year-over-year and is enabling consumers to begin rebuilding their savings. The personal savings rate bottomed out at a 17-year low in June 2022 at 2.7 percent. It has since improved to 4.6 percent, reflecting a more cautious consumer, but remains below pre-COVID levels that were closer to 9.0 percent.

The Lending Market

Leading Economic Indicators declined for the fourteenth consecutive month in May, suggesting that the huge rise in interest rates and tightening of bank lending standards will continue to cause the economy to slow as we move through 2023.

Reflecting tighter bank lending standards, loans and leases at all commercial banks have been flat from the end of February through the end of June. The outstanding level of bank credit has declined to levels last seen in August 2022, and much of the recent weakness has been in business C&I and consumer loans. Commercial real estate (CRE) has also slowed down markedly.

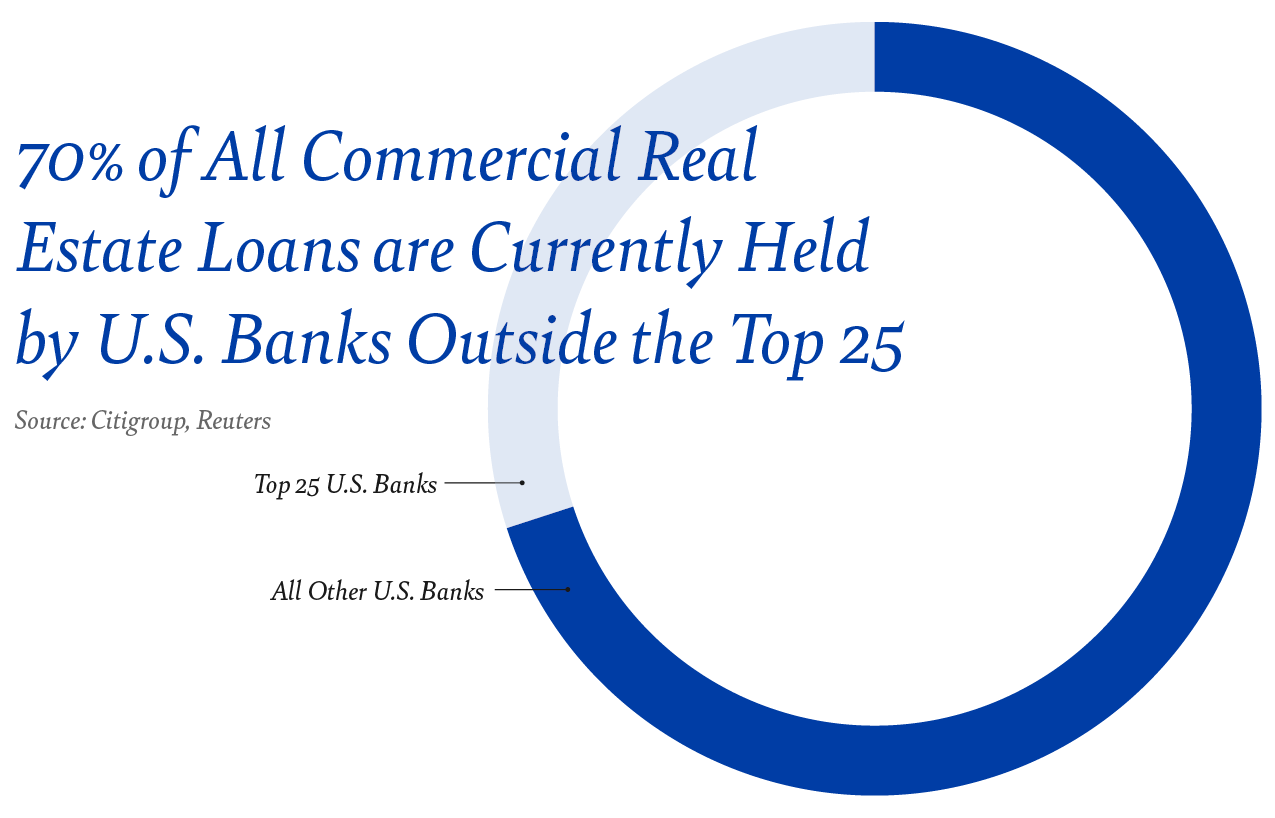

The results of the Fed’s annual stress tests showed that the big U.S. banks are generally in strong shape. However, with around 70 percent of CRE loans held by banks outside of the largest 25 banks, there is a risk that smaller banks with heavily concentrated CRE loan portfolios could yet run into trouble.

GDP & Industrial Production

The final revision for GDP in the first quarter was upgraded to 2.0 percent annualized growth from 1.3 percent, driven by a stronger contribution from net trade, with exports rising more strongly than previously thought, and import growth revised lower.

U.S. industrial production declined 0.2 percent in May for the first monthly decline of the year. The ISM manufacturing index reported its eighth consecutive reading below 50 (indicating contraction) at 46.0. On the other hand, the ISM services index rose to a four-month high of 53.9. The weighted average of the services and manufacturing indices is at a level consistent with flat GDP growth.

The latest surveys of capex intentions point to further declines in equipment investment, as the lagged impact of higher interest rates and the severe tightening of bank lending standards takes its toll.

Employment

The June establishment employment report showed an increase in non-farm payrolls of 209,000 – the weakest gain since December 2020. Additionally, the gains in the prior two months were revised down by 110,000. The household survey showed an increase of 273,000 and, with a small increase of the labor force of 133,000, the unemployment rate dipped from 3.7 percent to 3.6 percent. Interestingly, the household survey also showed an increase of 233,000 in people with multiple jobs – perhaps an indication that things are getting tighter. Wages increased 0.4 percent in June leaving the year-over-year figure at 4.4 percent – too high for the Fed.

The strength in the labor market over the past year has occurred while the economy has been slowing. The result is that productivity has been negative on a year-over-year basis since first quarter 2022.

Fed Funds Rate

Finally, the Fed held the Fed Funds target rate range at 5.00 percent to 5.25 percent at their June 14 meeting. This was the first pause by the Fed since the initiation of interest rate increases in March 2022, but their statement after the meeting made it clear that the pause was only to allow officials to “assess additional information and its implications for monetary policy.” At his recent testimony before Congress, Chair Powell described an economy that is still strong with inflation running too high, and repeated that most officials think interest rates will need to go higher to tame prices. The Fed’s most recent projections call for the Fed Funds rate rising to 5.6 percent by year-end. That’s an additional 50 basis points of tightening.

Markets are beginning to accept the Fed’s mantra that interest rates will remain higher for longer. A 25-basis point increase in the Fed Funds rate is now expected at the upcoming July 26 meeting, with the possibility of another hike by the end of the year. Expectations for the first decline in the Fed Funds rate have now been pushed out to mid-2024.

Insights

Research to help you make knowledgeable investment decisions