Rate volatility triggers refi opportunities

Conducting a loan portfolio analysis could reveal “trifecta” of financial incentives to refinance ahead of maturity dates.

CINCINNATI, OHIO (March 30, 2022) – On the heels of the long-anticipated Fed rate hike in mid-March – its first since 2018 – cost of capital is top-of-mind for real estate owners.

Capital markets have changed dramatically over the past two months due to rising rates and wider spreads created by external market forces. The 10-year treasury has climbed over 1.0% since 9/1/2021 and about 75 basis points in 2022 alone. In addition to its quarter point rate increase, the Federal Open Market Committee (FOMC) has signaled that the Fed will likely raise rates up to six more times this year and up to four times in 2023. Although that context is important, rate moves are never a sure thing. Frankly, no one has that crystal ball to say whether rates will move higher, when they could just as easily drop 30 or 40 basis points tomorrow.

One of the certainties of the current volatile environment is that now is an ideal time to review your portfolio and look at loans that might be maturing within the next three to four years, to see whether it makes sense to refinance. That analysis takes into consideration key factors – the ability to lock in a new low rate and pull cash out, while also weighing pre-payment premiums to determine how much an owner might save over the life of a new loan.

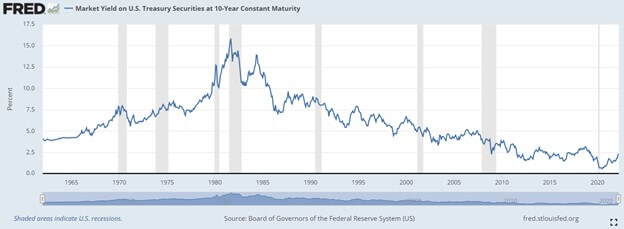

For example, Northmarq recently conducted a loan portfolio analysis for a client on eight different properties (self-storage and apartment). The analysis took a comprehensive look at pre-payments, current payments, future payments and cash out ability across different lender and loan product options. In this case, the pre-payment was a fixed 1% for the next three years. The client believes that rates are going up and recently moved forward with the the refinance of the first loan on a self-storage asset. The client was able to lock in the rate in the low 3% range on an IO loan, pull out several million dollars in equity and reduce the loan payment by $3,000 per month. That is a bit of a best-case scenario with a “trifecta” of incentives to refinance now. However, if the owner had not done the analysis, they would not have been aware of the opportunity. If you believe rates could substantially increase in the future, the cost to refinance early could easily be less than a higher-rate loan in the future. It is important to note, that comparatively speaking, we are still in a period of historically low rates. Figure 1 below depicts 10-year treasury rates since 1962. The 10-year treasury historic low occurred on August 4th, 2020, at 0.52% while the 10-year treasury high occurred on September 30th, 1981 at 15.84%. The historical average for the 10-year treasury since 1962 is 5.94% (with a median rate of 5.73%). The 10-year treasury today is above 2.40%

Despite rate volatility and speculation that rates could move higher, borrowers can still find attractive financing rates and lock in low rates for the next 10 or 20 years. Although lenders are shying away from risk, they are willing to lend on all property types, including stepping back into retail, office and, in some cases, hospitality.

Borrowers will benefit from life insurance company loans which offer early rate locks (at term sheet or loan application) which the lender can hold for 3-6 months at no additional premium. Some lenders are willing to hold a rate even longer, for 9-12 months, which delivers the added benefit of reducing any prepayment penalty. Holding that rate for a longer period does come with a slight premium, 2 to 5 basis points per month past three or four months. However, the upside is that it may allow you to reduce your prepayment penalty and provides the added benefit of holding your rate in a rising rate environment.

Another incentive fueling refi opportunities is the strong value appreciation that many property owners have experienced. Property cash flow and values have increased significantly over the last 5-10 years. However, if an owner decides to sell an asset to realize gains, it creates a question of what to do with the sale proceeds. Can you reinvest in today’s competitive marketplace and successfully complete a 1031 exchange, or could you potentially face a tax on the gain? A big advantage of a cash-out on a refi is that those proceeds are tax free, and you also continue to generate cash flow from the property.

Oftentimes, borrowers put long-term, fixed-rate debt on a property and forget about it until that loan is about to expire. That is even more true in what has been a long-running period of historically low interest rates. Now that the rate environment is starting to shift, it is a good time to conduct a financial analysis of loans with maturities through 2025 to determine if there are any opportunities to refinance. The best advice is to work with a service provider, such as Northmarq, that has the expertise and access to up-to-the-minute market data to run a comprehensive analysis with customized solutions.

Fig. 1

Insights

Research to help you make knowledgeable investment decisions